A number of companies listed on the Australian Securities Exchange (ASX) can expect to be captured by new mandatory sustainability reporting requirements as of this financial year. This update provides a summary of which companies this impacts and what must be reported.

Annual Reporting Requirements

Currently, Australian companies listed on the ASX are required to:

- Provide the ASX with its audited accounts for the full financial year when lodging with the Australian Securities and Investments Commission (ASIC), in any case no later than three months from the end of its financial year; and

- Prepare and send an annual report to its shareholders within four months from the end of its financial year.

Moving forward, ASX-listed companies may now be captured by the new mandatory requirements which require the preparation of a sustainability report (Sustainability Reporting Requirements).1

Which ASX-Listed Companies Are Required to Prepare Sustainability Reports?

ASX-listed companies are required to prepare and lodge financial reports under Chapter 2M (being the financial reporting provisions) of the Corporations Act 2001 (Cth). Accordingly, the Sustainability Reporting Requirements will apply if an ASX-listed company falls within one of the following groups 2 :

Group 1:

- Companies meeting at least two of the following criteria for the relevant financial year:

- consolidated revenue of more than AU$500 million;

- consolidated gross assets of more than AU$1 billion; or

- 500 or more employees, or

- Companies above the threshold in section 13(1)(a) of the National Greenhouse and Energy Reporting Act 2007.

Group 2:

- Companies meeting at least two of the following criteria for the relevant financial year:

- consolidated revenue of more than AU$200 million;

- consolidated gross assets of more than AU$500 million; or

- 250 or more employees, or

- Companies subject to other National Greenhouse and Energy Reporting Act 2007 reporting obligations.

Group 3:

- Companies meeting at least two of the following criteria for the relevant financial year:

- consolidated revenue of more than AU$50 million;

- consolidated gross assets of more than AU$25 million; or

- 100 or more employees.

Deadlines

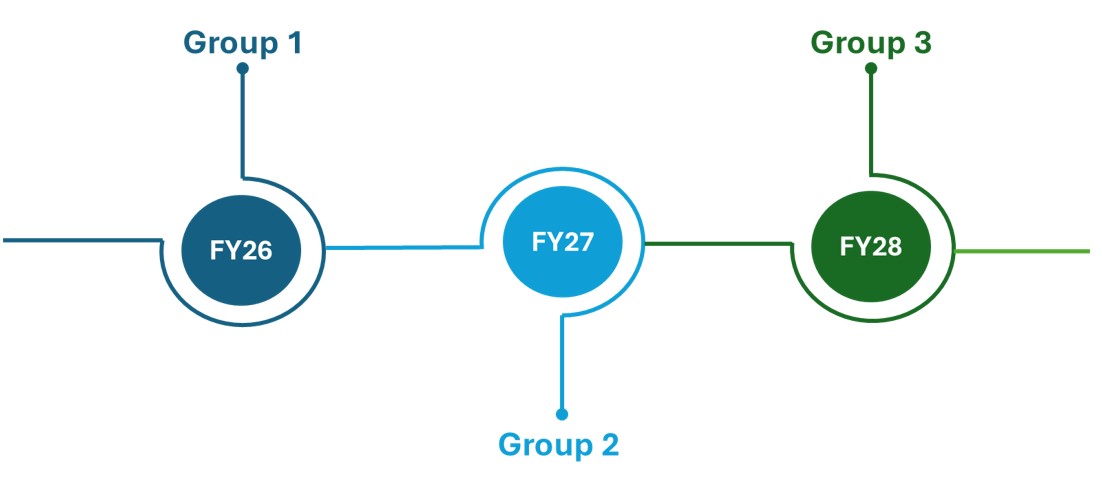

The first financial year in which Group 1, 2 and 3 companies must comply with the Sustainability Reporting Requirements is set out in the timeline below:

Source: K&L Gates

Accordingly, the first phase of climate-related disclosures for Group 1 companies is due this financial year ending 30 June 2026.

What Must Be Reported?

The Sustainability Reporting Requirements include preparing:

- Climate statements for the year;

- Any notes to the climate statements; and

- The directors’ declaration regarding the statements and notes,

which must include:

- Material financial risks and material financial opportunities relating to climate;

- Metrics and targets relating to climate, including those relating to Scope 1, Scope 2 and Scope 3 greenhouse gas emissions; and

- Information relating to the governance or strategy of, or risk management by the company in relation to, the above.

If a Group 3 company determines that it has no material climate-related risks or opportunities for that financial year, its climate statement must state this and an explanation as to how it came to this conclusion.

ASX Lodgement

The timing for providing ASX with a sustainability report for an ASX-listed company coincides with lodgement of its annual reporting documents as required by Listing Rule 4.5 (being no later than three months after the end of the financial year).

However, late lodgement of a sustainability report will not automatically result in mandatory suspension from trading on the ASX (as a result of amendments made by the ASX to Listing Rule 17.5).

Next Steps

As the Sustainability Reporting Requirements are being phased in over three years, ASX-listed companies should begin preparing to ensure compliance ahead of each relevant deadline.

1 As introduced by the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 (Cth).

2 Separate thresholds apply for superannuation funds and managed investment scheme entities.

The author would like to thank graduate Cleo Taliadoros for her contributions to this alert.